Want To Pay Off Your Home Faster? Here’s What Two Extra Payments A Year Can Do

September 2, 2025

Key Takeaways:

- How Extra Payments Can Reduce Mortgage Terms: Learn how adding two extra mortgage payments annually can shrink your loan term and lower the total interest paid.

- What to Know About Prepayment Penalties: Before making extra payments, check for prepayment penalties in your loan agreement. Understanding these terms can help you avoid unexpected fees and make smarter decisions about how and when to pay.

- Adjusting Your Amortization Schedule with Extra Payments: Explore how extra payments reshape your loan schedule, reduce long-term interest, and push your payoff date forward.

If you own a home in Texas, you already know that few things feel as rewarding as tackling your mortgage. However, homeownership thrills can be quickly overshadowed by the reality of a 30-year loan and years of interest piling up. But what if you could take control, save thousands of dollars, and pay your home off years ahead of schedule? For many Texas homeowners, making two extra mortgage payments a year is a powerful strategy that promises long-term financial rewards.

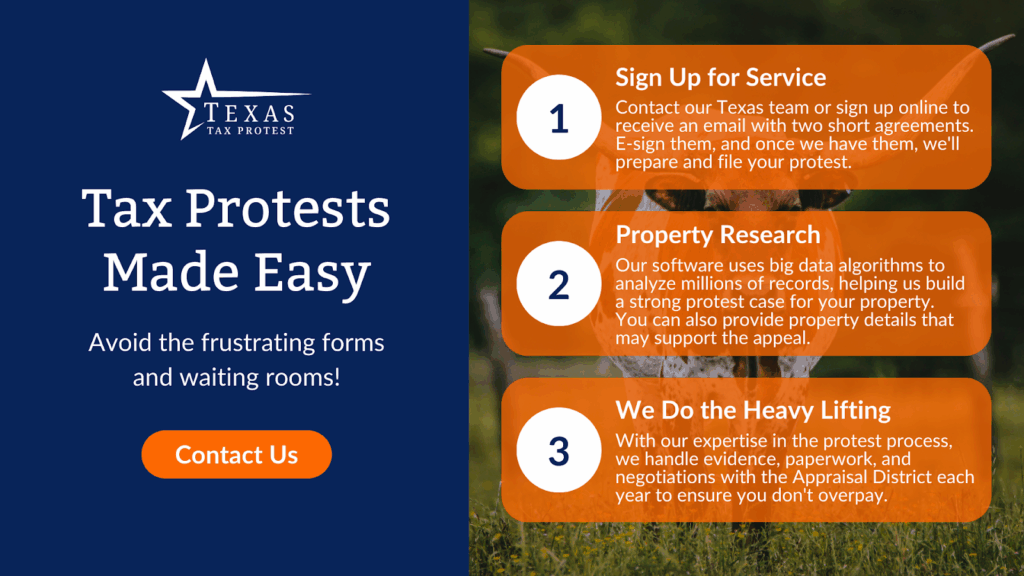

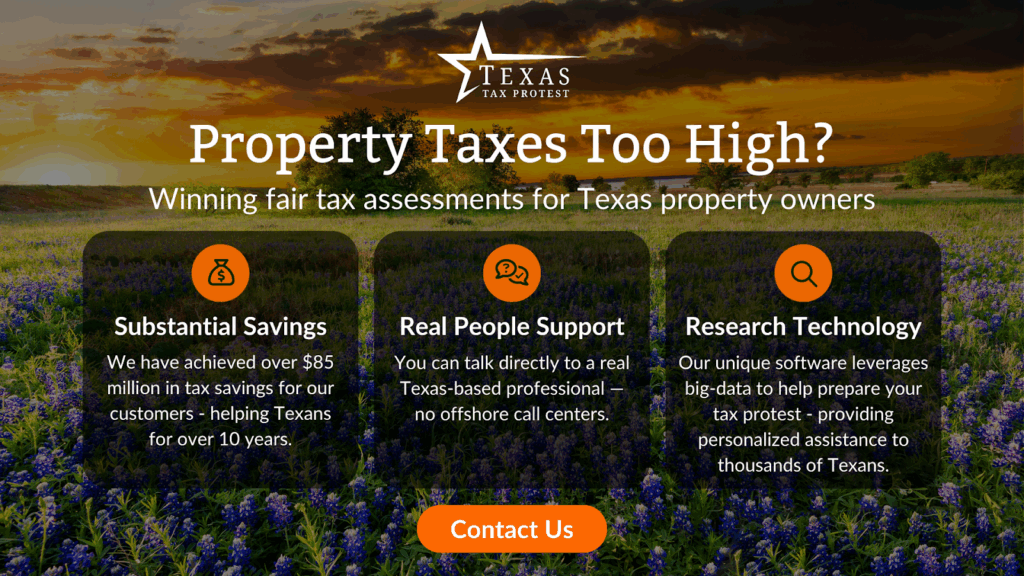

At Texas Tax Protest, we’re here to help you make the most of every dollar, whether in your mortgage planning or your next property tax protest. This guide breaks down how extra payments work, how much you could save, and how to decide if this approach aligns with your financial goals.

How Two Extra Payments A Year Can Reduce Your Mortgage Term

Adding just two extra mortgage payments per year can dramatically reduce the time it takes to own your home outright. This simple strategy works by sending more money to your loan’s principal, which reduces the amount of interest you’ll owe and speeds up your payoff timeline.

More Of Your Money Goes Toward Principal

Your mortgage principal is the amount you originally borrowed to buy your home. That number shrinks over time as you make payments, but in the beginning, most of each monthly payment goes toward interest, not the loan balance. That’s because interest is calculated based on what you still owe. So the higher your remaining balance, the more you’ll pay in interest month after month.

When you make extra payments and apply them directly to your principal, you reduce the loan balance faster. That means less interest gets added over time, and more of your regular payments start going to the principal instead of interest. The earlier in your loan you start, the more powerful this shift becomes.

A Simple Example Of Two Extra Payments In Action

Consider a homeowner with a $325,000 mortgage at a 6.5% fixed interest rate. By making just two extra payments per year—added on top of regular monthly payments—they could shorten the loan term by more than five years. That change alone may result in savings of over $60,000 in interest, depending on how early the extra payments begin and how consistently they’re made.

This happens because every extra dollar sent to the principal immediately reduces the amount the lender can charge interest on. Over time, those accelerated contributions build momentum. Even small, consistent payments add up in meaningful ways.

How Biweekly Payments Create Long-Term Savings

Some homeowners choose a biweekly schedule instead of making two larger extra payments. Rather than sending one full payment each month, they divide the amount in half and pay every two weeks. Since there are 52 weeks in a year, this results in 26 half-payments, or 13 full ones.

That extra payment might not feel significant at first, but it creates steady progress. For example, if your regular monthly payment is $2,000, making biweekly payments of $1,000 means you’ll contribute $26,000 over the year. That adds up to one additional full payment beyond what’s required—and just like a lump sum, that payment helps cut down the principal and the interest that follows.

Why Escrow Doesn’t Reduce Your Loan Balance

Mortgage payments often include more than just principal and interest. Most lenders collect additional funds in what’s called an escrow account. This money is set aside to pay property taxes and homeowners’ insurance on your behalf. While it’s helpful to have those costs covered automatically, escrow contributions don’t help reduce your loan.

In other words, extra money sent to escrow won’t speed up your mortgage payoff or reduce how much interest you owe. To make progress toward owning your home faster, your additional payments need to go straight to the principal. Some lenders apply extra funds to future interest or escrow by default, so it’s important to be specific.

Prepayment Penalties: What You Need To Know

Paying off your mortgage early might sound like a win, but depending on your loan agreement, doing so could trigger a fee. These charges can complicate an otherwise smart financial move. Before you commit to a new payment plan or extra contributions, it’s worth learning how these fees work and where they may show up in your mortgage paperwork.

Why Some Lenders Charge A Penalty For Paying Early

Lenders collect most of their profit from the interest that builds up over time. When homeowners make extra payments or pay off their mortgage ahead of schedule, that interest stream gets cut short. To protect that income, some lenders might include a prepayment penalty in the loan terms.

When And Where To Look For Prepayment Clauses

These penalties are not universal, and in Texas, they’re less common than in some other states. Still, they appear in certain loan agreements, especially newer mortgages or those issued through specialized financing programs. To find out if your mortgage includes a prepayment clause, dig into your closing documents. There should be a section labeled “prepayment penalty” or “prepayment provision” in your paperwork. This section outlines if a penalty applies, how long the clause lasts, and what triggers the fee.

How Prepayment Fees Are Calculated

Prepayment penalties come in a few different forms. Some loans include a flat fee. Others use a percentage of your remaining loan balance. In some cases, the fee is based on how much interest the lender would have collected if you’d stuck to the original payment schedule.

For example, if your loan has a 3% early payoff penalty and you owe $200,000, the fee could cost you $6,000. But in another scenario, the penalty might only apply to payments made in the first three years and disappear after that window closes. Since the terms vary widely, running the numbers before making extra payments helps you decide what’s worth it.

Why Prepayment Penalties Matter For Your Strategy

Learning whether your mortgage includes a prepayment penalty helps you plan smarter. A surprise fee can take the shine off your early payoff goals. But with the right information, you can weigh the tradeoffs and decide if extra payments are still the best move. Before adjusting your payment plan or committing to a biweekly schedule, review the terms in your loan documents and confirm how additional payments will be handled. A quick call to your lender can clear up anything that feels vague and help you avoid unexpected charges.

Adjusting Your Amortization Schedule With Extra Payments

Amortization refers to how your mortgage is paid off over time, with each monthly payment covering a portion of the interest and principal. In the early years of your loan, most of your payment goes toward interest. As the balance decreases, more of your payment is applied to the principal. Adding extra payments throughout the year gives you the power to shift that timeline in your favor. Here’s how:

- Extra payments go straight to principal: When you send more than the required monthly amount and request that it be applied to the principal, you reduce the balance faster. That creates a ripple effect by lowering the interest charged on future payments.

- Interest is calculated on a smaller balance: Because lenders calculate interest based on what you still owe, knocking down the balance early in the loan term reduces the total interest over time.

- You can shorten your loan term by several years: For example, on a $300,000 mortgage with a 30-year term and a 6.5% interest rate, making just two extra payments per year can cut five or more years off your loan and result in tens of thousands in savings.

- Online amortization calculators show the impact: Plug your numbers into a mortgage calculator and apply extra payments to see how they change the payoff timeline. Each early contribution pushes your payoff date forward.

- Most lenders apply extra payments correctly: Many lenders default extra payments to future interest or escrow unless you specify otherwise. Include a note or call ahead to confirm that those funds will reduce your principal directly.

- Mortgage-free doesn’t mean cost-free: Even once the loan is paid off, Texas homeowners still cover annual property taxes and insurance. But paying off the mortgage early helps create room in your budget and lowers the long-term cost of owning your home.

Final Thoughts

Paying two extra mortgage payments a year is a powerful financial strategy with real impact. Those extra payments can dramatically reduce the lifetime interest you’ll pay and help you own your home years sooner. Getting ahead on your loan also positions you well if you’re looking to free up cash for other life goals or simply want the peace of mind from reducing debt faster.

Of course, homeownership in Texas involves more than paying off the loan. Property taxes remain a significant part of your yearly costs. At Texas Tax Protest, we know every dollar counts. That’s why we’re committed to helping homeowners maximize all available savings by giving you the tools and advocacy needed for fair property tax assessments. Our blend of technology and personalized service helps keep your costs in check, so you can focus on what matters most: getting the full value out of your home.

Read more:

- Texas Property Tax Rates Explained: What Every Homeowner Should Know

- Texas Property Tax Rates by City: Where Does Your Area Rank?

- Texas Disaster Declarations and How They Impact Your Property Taxes

Frequently Asked Questions About Making Two Extra Mortgage Payments A Year

How does making two extra mortgage payments a year help pay off my home faster?

Adding two extra mortgage payments each year, beyond your regular monthly installments, directly reduces the loan principal faster than scheduled. This means less interest will accrue over time, potentially shaving years off your mortgage and saving thousands in interest. Even small, consistent extra payments make a big difference toward your financial freedom.

What is the impact of biweekly payments on my mortgage?

Switching to biweekly payments means you make half your monthly payment every two weeks. Since there are 52 weeks in a year, this results in 26 half-payments, or effectively 13 full payments annually—one extra payment than the standard 12. This method steadily chips away at your mortgage principal, accelerating your payoff schedule and reducing total interest.

Is it better to make extra payments towards the principal or escrow?

Directing extra payments toward your principal has the biggest impact on paying off your mortgage early. Extra payments to escrow won’t reduce your loan balance; they only cover property taxes and insurance. Always specify that your extra payment is “principal only” when sending it—double-check with your lender’s process to avoid confusion.

Should I consult with my lender before making additional mortgage payments?

Absolutely. Some lenders have specific instructions for processing extra payments, and a quick conversation makes sure your money goes toward paying down the principal, not prepaying interest or escrow. You can also confirm there aren’t any prepayment penalties and learn about your options for scheduling additional payments.

How do I budget for making an extra two mortgage payments annually?

Many homeowners find success with incremental savings—setting aside a small amount each month that adds up to a full payment or two by year’s end. Alternatively, allocating part of bonuses, tax refunds, or other windfalls works well. The key is building extra payments into your budget sustainably, without straining your finances.

Should I focus on paying off other debts before making extra mortgage payments?

Take a close look at your other debts, especially those with high interest rates, like credit cards or personal loans. Prioritizing higher-interest debt usually makes more sense, as it saves you more money long-term. Once those are handled, ramping up mortgage payments is a smart next step.

What are the tax implications of making extra mortgage payments?

Mortgage interest is generally tax-deductible, but as your principal balance drops faster, you’ll pay—and deduct—less interest over time. This could mean a slightly smaller mortgage interest deduction each year. For questions about your specific situation and maximizing tax benefits, it’s always wise to consult a tax professional or advisor familiar with Texas property tax laws.

What should I do if my financial situation changes after I start making extra payments?

Stay flexible. If you need to pause or scale back extra payments due to a change in income or unexpected expenses, reach out to your lender and review your budget. You can always increase payments again later when circumstances improve. Curious about other ways to take control of your homeownership costs? At Texas Tax Protest, we help Texans just like you find savings and strategies for smarter property tax management.

Most Recent Blogs

December 11, 2025

Texas Voters Approve Historic Property Tax Relief Through Constitutional Amendments

Texas Tax Protest breaks down the newly passed Texas tax relief amendment, explaining its impact on property owners and what it means moving forward.

Read BlogDecember 10, 2025

Texas Property Tax Cuts: What The November 2025 Election Results Mean For Homeowners And Businesses

Texas Tax Protest breaks down the 2025 Texas property tax cuts and election results, revealing what homeowners and businesses need to prepare for in 2026.

Read BlogNovember 10, 2025

Protest Your Austin Property Taxes with Texas Tax Protest

At Texas Tax Protest, we help Austin property owners reduce tax burdens through effective protests. Learn more and contact our team today!

Read BlogNovember 10, 2025

Protest Your San Antonio Property Taxes with Texas Tax Protest

Property taxes in San Antonio can be a heavy financial burden for property owners. Learn how to lower your tax bill with Texas Tax Protest.

Read BlogNovember 10, 2025

Protest Your Houston Property Taxes with Texas Tax Protest

At Texas Tax Protest, we specialize in helping Houston property owners reduce property taxes through successful protests. Learn how today!

Read BlogNovember 10, 2025

Protest Your Fort Worth Property Taxes with Texas Tax Protest

Property taxes in Fort Worth can place a burden every tax season. Fortunately, property taxes can be reduced with a successful protest.

Read Blog4.2

All rights reserved.